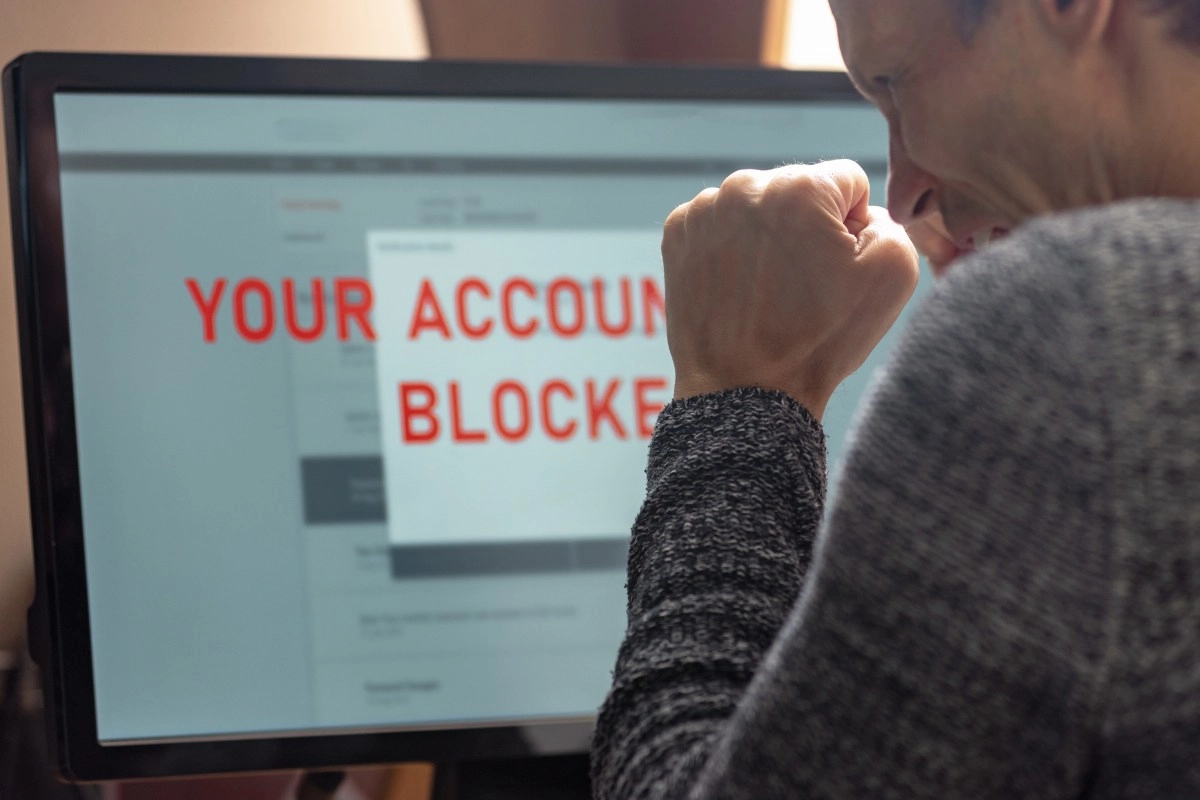

No one expects that, when logging into their account to make a payment, they will find the bad news that it has been rejected despite being clear that they had sufficient funds to do so. The surprise of finding your account frozen when you have no outstanding debts is more common than you imagine. Therefore, we are going to explain to you what happens in these situations and what you can do to recover the availability of your money.

This type of situation is usually related to a procedure known as bank seizure. This is a legal tool that allows certain creditors to recover money owed through a court order. The problem is that sometimes administrative errors, similar names, outdated information, or even cases of identity theft can cause the affected account to be incorrect.

What happens when they freeze the wrong account?

When a financial institution receives a valid court order to freeze funds, it typically must comply immediately. In most cases, the bank does not first check for an error; The block is simply applied and any claims that may arise are then reviewed.

This means that a person completely unaware of the debt could be temporarily left without access to some or even all of your money. During that time, automatic payments could fail and result in late fees, overdraft fees, or penalties.

For example, if you share a similar name with another person or if your information was mixed up in a registry, you could find yourself involved in a process that has nothing to do with you.

What can you do if your bank account is frozen by mistake?

Although frustrating, it is generally up to the account holder to prove that the lien was incorrectly applied. The first thing is to contact the bank to obtain details about the order that caused the block.

It may then be necessary to contact the collection agency and, in some cases, the court that issued the court order.

In this dispute process, you need to prove with documents that you have no relationship with the debt that is attributed to you. They may ask you for official identification, account statements, proof of ownership or any evidence that shows that you are not the person identified in the debt.

The faster you act, the greater the chances of solving the problem in less time. Waiting several days or weeks can complicate the process and prolong restricted access to your funds.

Some funds have special protection

Not all money deposited in an account can be seized in the same way. There are certain incomes that are protected under federal law. These include some Social Security Administration (SSA) benefits, Supplemental Security Income (SSI), veterans benefits, and other specific government payments.

Banks typically review whether an account receives these types of protected deposits before fully enforcing a garnishment. However, errors can also occur. If you consider that protected funds have been frozen, you must provide evidence that proves the origin of those resources.

Can you recover the lost money?

Depending on the circumstances, you may be entitled to compensation for financial damages caused by an erroneous seizure. For example, if the blocking resulted in declined payment fees, bank fees, fines, or any other demonstrable financial loss, you may be able to claim those damages.

That is why it is important to preserve all documents related to the case. Save emails, letters, screenshots, payment receipts, and records of any additional expenses generated by the account lock.

What if the embargo turns out to be legitimate?

Sometimes a person believes there is a mistake, but later discovers that the debt is owed and that the court order is valid. In this scenario, instead of challenging the embargo, it is advisable to look for alternatives to resolve the debt and avoid future blockages.

Options available include direct negotiation with the creditor, debt management plans offered by credit counseling agencies, and, in more complex situations, bankruptcy.

Each alternative has advantages and disadvantages: some can affect credit history or have long-term financial consequences. However, they often offer more control than ignoring the problem and allowing foreclosures to continue.

You may also be interested in: